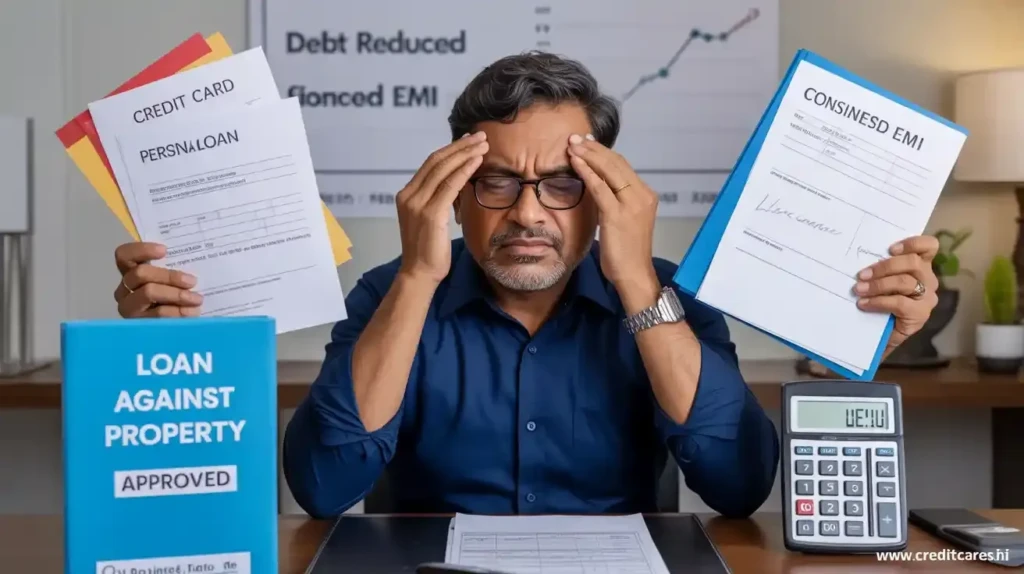

Managing multiple loans with different EMIs and interest rates can become overwhelming. For many Indian borrowers, especially business owners, Loan Against Property (LAP) provides a smart, structured way to consolidate debts and improve financial health. Let’s explore how this works and why it might be the right strategy for you.

What Is a Loan Against Property (LAP)?

A Loan Against Property is a secured loan where you pledge a residential, commercial, or industrial property as collateral to raise funds. This type of loan offers lower interest rates and longer repayment tenures compared to personal loans or credit card debt.

According to the Reserve Bank of India, LAP is governed under general lending norms, and banks assess the borrower’s repayment capacity, credit profile, and property value before sanctioning the loan.

You can learn more about secured loans and collateral requirements on Investopedia.

Why Use LAP to Consolidate Debt?

1. Lower Interest Rates

LAP interest rates range from 9%–12%, significantly lower than credit card interest (30–40%) or personal loans (14–24%).

Visit HDFC Bank’s LAP page or SBI LAP details to compare rates.

2. Single EMI Instead of Many

Instead of juggling 4–5 loans, LAP lets you combine all liabilities into one. This simplifies your cash flow and reduces the risk of missed payments.

Check the benefits of debt consolidation in CIBIL’s financial literacy section.

How LAP Helps in Debt Consolidation

Here’s how the process works:

-

✅ Assess total outstanding debts (personal loan, credit cards, gold loan, etc.)

-

✅ Apply for LAP based on your property value and income

-

✅ Use LAP disbursed amount to pay off all existing debts

-

✅ Start repaying the LAP in easy EMIs at a lower rate

For example, if you owe ₹10 lakhs across 3 loans at 20% average interest, you can repay it using LAP at just 10.5%, saving lakhs over time.

Use ICICI Bank’s LAP EMI calculator to estimate your monthly outflow.

Eligibility for LAP for Debt Consolidation

Most salaried professionals, business owners, and self-employed individuals are eligible. Here’s what lenders typically check:

-

Clear property title

-

Repayment capacity (based on ITR, bank statements)

-

CIBIL score (ideally 700+)

To understand your eligibility, refer to Bajaj Finserv’s LAP criteria or Axis Bank LAP guide.

Documents Required

-

PAN and Aadhaar

-

Income proof (ITR, bank statement)

-

Property documents

-

Existing loan details (if applicable)

Check the full checklist on Bank of Baroda’s LAP documentation page.

Risks and Things to Keep in Mind

-

Property at risk: Defaulting can lead to legal action and auction of your property.

-

Processing time: LAP approval may take longer than unsecured loans (7–14 days).

-

Value cap: Most banks lend only up to 60–70% of your property’s market value.

Learn about property loan risks on NHB’s consumer awareness portal.

Real-World Example

Let’s say a Delhi-based shop owner owes ₹8 lakhs split across a business loan (₹3L), personal loan (₹2L), and credit card (₹3L). He pledges his ₹40L residential flat and gets a ₹12L LAP at 10% over 10 years. He clears all old dues and now pays just one EMI of ~₹16,000/month – much lower than earlier combined EMIs of ₹27,000.

Use RBI’s EMI calculator to plan your own repayment schedule.

FAQs

1. Can I consolidate business and personal loans using LAP?

Yes, LAP funds are flexible. You can use them for personal, business, or medical debt consolidation. Refer to HDFC’s LAP use cases.

2. Will my CIBIL score improve if I consolidate debt using LAP?

Absolutely. Paying off existing high-interest debts through LAP can boost your CIBIL score over time, provided you repay LAP EMIs on time.

3. Can I foreclose a LAP early?

Yes, most banks allow foreclosure after a minimum lock-in. Check for prepayment penalties in your loan agreement or with SBI’s foreclosure rules.

4. Is co-applying with spouse or parent allowed in LAP?

Yes, joint ownership and co-application often help increase loan eligibility. See Kotak Mahindra’s joint LAP benefits.

5. Can LAP be used to pay off home loan or gold loan?

Yes. LAP proceeds can be used for any legitimate financial obligation including home loans, education loans, or gold loans. See RBL Bank’s LAP FAQs.

Conclusion

Using a Loan Against Property to consolidate your existing debts is a smart and secure financial decision for those with stable income and valid property ownership. It reduces interest burden, simplifies your repayments, and helps rebuild your credit score.

If you’re unsure about eligibility or EMI, consult with our experts to check your LAP eligibility now.