Balance Transfer + Top-Up Loan: Cut Your EMI and Get More

Written by CreditCares Advisory Team — Reviewed by Senior Credit Advisor, CreditCares

Reducing a ₹50 lakh business loan from 14% to 11.5% across the remaining 4-year tenure saves roughly ₹2.7 lakh in interest — without changing anything about your collateral, your business, or your repayment discipline. That is what a balance transfer does. Pair it with a top-up, and you walk away with fresh capital at the same time.

A balance transfer + top-up loan is a two-part transaction: the outstanding principal on your existing loan shifts to a new lender at a lower rate, and the same new lender sanctions additional funds over and above that outstanding amount — all under one facility, one set of documents, and one EMI.

This guide covers how the product works, when the numbers actually favour a switch, what lenders check, and the one calculation most borrowers skip — the break-even period — that determines whether any balance transfer is genuinely worth doing.

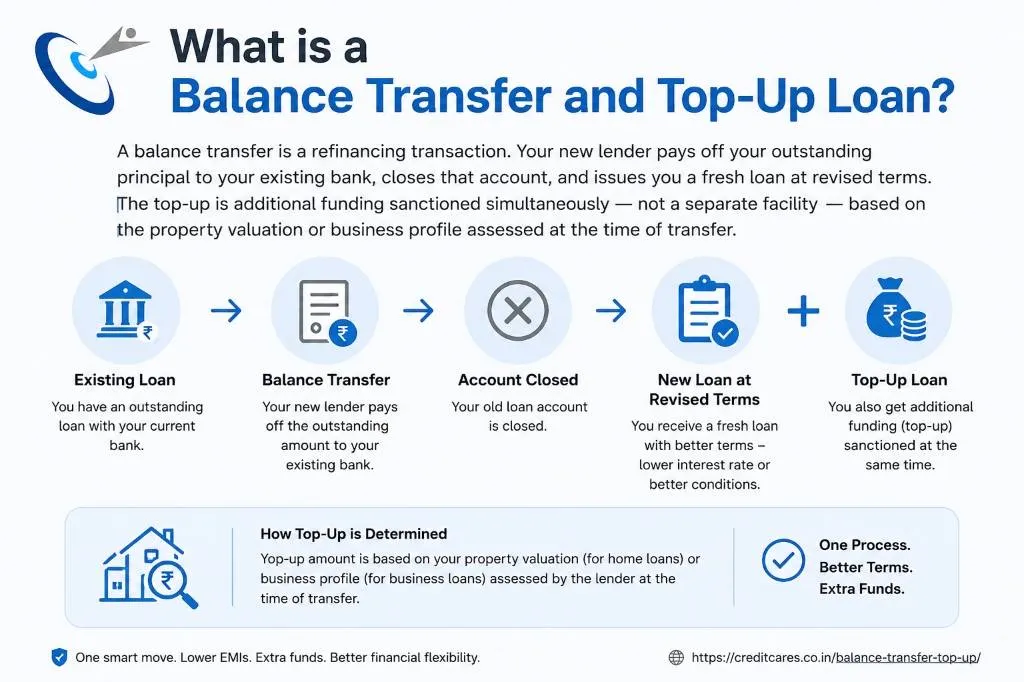

What is a Balance Transfer and Top-Up Loan?

A balance transfer is a refinancing transaction. Your new lender pays off your outstanding principal to your existing bank, closes that account, and issues you a fresh loan at revised terms. The top-up is additional funding sanctioned simultaneously — not a separate facility — based on the property valuation or business profile assessed at the time of transfer.

The most common products eligible for this combination in the Indian commercial lending space are:

| Loan Type | Balance Transfer Eligible? | Top-Up Typically Available? |

|---|---|---|

| Business term loan | Yes | Yes (unsecured or LAP-backed) |

| Loan Against Property (LAP) | Yes | Yes (based on updated property value) |

| Working capital term loan | Yes | Case-by-case |

| Cash Credit/overdraft | Rarely — structure differs | Usually converted to term loan first |

| Equipment/machinery loan | Yes | Limited |

The top-up component on a LAP balance transfer is particularly powerful. If property values have risen since your original loan was sanctioned, the updated valuation may support a significantly larger total facility than your original sanction — giving you a rate reduction and new capital simultaneously.

When Does a Balance Transfer Make Financial Sense?

The decision comes down to one number: the break-even period.

The break-even period is the number of months it takes for your cumulative monthly EMI savings to equal all the costs you pay upfront to switch lenders.

Break-even (months) = Total transfer costs ÷ Monthly EMI saving

Total transfer costs include:

- Foreclosure/prepayment charges from your existing lender (typically 1–3% of outstanding principal for business loans; nil for floating-rate loans to individuals and eligible MSMEs under RBI guidelines — verify your specific loan terms).

- Processing fee at the new lender (typically 0.5–2% of the transferred amount).

- Legal and valuation charges (for LAP, typically ₹10,000–₹40,000).

- Stamp duty on the new loan agreement (state-specific — in West Bengal, verify current rates).

- Administrative and documentation charges.

A Howrah-based engineering unit has an outstanding LAP balance of ₹45 lakh at 13.5% with 5 years remaining. A new lender offers 11% for the same tenure.

- Current EMI (approx.): ₹1,04,000/month

- New EMI (approx.): ₹97,000/month

- Monthly saving: ₹7,000

- Total transfer costs (illustrative): ₹90,000 (foreclosure + processing + legal)

- Break-even: 90,000 ÷ 7,000 = ~13 months

If you have more than 13 months remaining on the original tenure — which in this case is 5 years — the transfer is financially sound. If the break-even were 30 months on a 3-year remaining tenure, the numbers would not work.

General rule: A balance transfer makes sense when the break-even is less than half the remaining loan tenure.

Almost every article about balance transfers tells you to compare interest rates. What they don't tell you is that rate comparison alone misleads you when you are past the midpoint of your loan tenure.

Business loans and LAP are typically structured on reducing-balance EMIs. The interest component is highest in the early months and declines as the principal reduces. By the time you are two-thirds through a loan tenure, most of your remaining EMIs are principal repayment, not interest. Switching at this stage — even for a 2% rate reduction — may save you very little on interest while costing you full processing fees and foreclosure charges on the new facility.

Before approaching any lender for a balance transfer, ask your current lender for an amortisation schedule and check what proportion of your remaining EMIs is interest versus principal. If more than 70% of the remaining outflow is principal, the balance transfer arithmetic usually does not work in your favour regardless of the rate offered.

What Does a Balance Transfer + Top-Up Cost You?

A realistic cost structure for a business LAP balance transfer in 2026:

| Cost Component | Who Charges It | Typical Range |

|---|---|---|

| Foreclosure/prepayment | Existing lender | 0%–3% of outstanding principal + GST |

| Processing fee | New lender | 0.5%–2% of loan amount + GST |

| Legal charges | New lender's empanelled lawyer | ₹10,000–₹40,000 |

| Property valuation fee | New lender's empanelled valuer | ₹5,000–₹20,000 |

| Stamp duty on loan agreement | State government | Varies by state and loan amount |

| CERSAI registration | New lender (passed to borrower) | ₹50–₹200 (nominal) |

RBI Note on Foreclosure Charges: For floating-rate term loans sanctioned to individuals and eligible micro and small enterprises, the RBI has issued guidance restricting foreclosure charges. However, this does not automatically apply to all business loans — the applicability depends on the borrower category, loan type, and whether the rate is genuinely floating or effectively fixed. Confirm this with your existing lender before calculating your total transfer cost.

Eligibility: What the New Lender Checks

A balance transfer is treated as a fresh loan application by the new lender. They will assess:

- Repayment track record: Minimum 6–12 EMIs paid on time with your existing lender — most lenders ask for the last 12 months' loan statement showing clean repayment. A single EMI delay in the recent 6 months can result in rejection or a higher rate offer.

- CIBIL / credit score: A score of 700 or above is typically required for business owners. For LAP-backed transfers, some lenders go down to 680 if the property quality is strong.

- Business financials: Last 2–3 years of ITR, audited P&L and balance sheet, and GST returns for the periods not covered by the latest ITR. The new lender recalculates DSCR (Debt Service Coverage Ratio) — typically requiring a minimum of 1.25x — based on current income, not what was assessed at your original sanction.

- Property valuation (for LAP): The new lender sends their own empanelled valuer. If property values in your area have risen, this is where the top-up headroom is determined. The total facility (transferred balance + top-up) cannot exceed the LTV (Loan-to-Value) threshold set by RBI — 75% for residential property and 60% for commercial property in most cases.

- Existing lender's documentation: You will need the original sanction letter, the last 12 months' loan statement, and — once approved — a foreclosure letter and NOC (No Objection Certificate) from your existing lender. Collecting the foreclosure letter typically takes 7–15 working days; factor this into your timeline.

Documents Required for a Balance Transfer + Top-Up

| Document Category | Specific Items Required |

|---|---|

| KYC | PAN, Aadhaar, address proof (for proprietors and directors personally) |

| Business Identity | GST registration certificate, Udyam registration (if applicable), company incorporation documents |

| Financial Statements | Last 2–3 years ITR with computation, audited P&L and balance sheet, GST returns |

| Banking | Last 12 months' current account statements (all active accounts) |

| Existing Loan Documents | Original sanction letter, last 12 months' loan account statement, amortisation schedule |

| Property Documents (LAP) | Original title deed chain, latest property tax receipt, approved building plan, encumbrance certificate |

| From Existing Lender | Foreclosure letter with outstanding amount (collected after new lender's in-principle approval) |

The Top-Up Component: How Much Extra Can You Get?

The top-up amount depends on the gap between the current outstanding and the maximum the new lender can sanction against the property or business profile.

For LAP balance transfers: If your original LAP was ₹40 lakh on a property then valued at ₹70 lakh (57% LTV), and the same property is now independently valued at ₹90 lakh, the new lender's maximum at 60% LTV would be ₹54 lakh — giving you up to ₹14 lakh as a top-up over the outstanding ₹40 lakh.

(Note: This is an illustrative scenario only. Actual top-up eligibility depends on the updated valuation, borrower income, DSCR, lender policy, and property type.)

Disclaimer: Loan terms, interest rates, valuation norms, and processing charges mentioned above are indicative and subject to change by individual lending institutions. CreditCares is an independent financial advisory consultancy and DSA, not a direct lender. We do not guarantee balance transfer or top-up loan approvals; final credit terms are determined solely by the underwriting bank or NBFC. Please verify current rates and charges before executing any transfer agreements.