Term Loan for Business in India: Eligibility, Rates, and Documents (2026 Guide)

Written by the CreditCares Team — finance professionals, loan consultants, and credit experts with 12+ years of experience arranging business and healthcare financing across India.

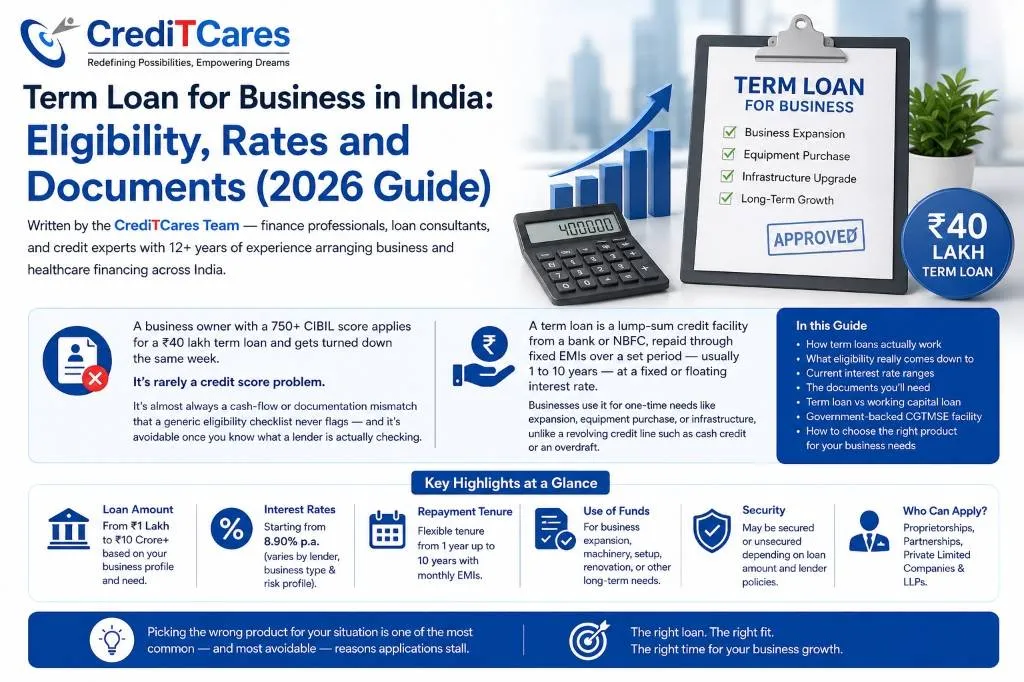

Imagine a business owner with a 750+ CIBIL score applying for a ₹40 lakh term loan, only to get turned down the same week. Surprisingly, it's rarely a credit score problem. It's almost always a cash-flow or documentation mismatch that a generic eligibility checklist never flags—and it's avoidable once you know what a lender is actually checking.

Unlike a revolving credit line such as cash credit or an overdraft, a term loan is a lump-sum credit facility from a bank or NBFC, repaid through fixed EMIs over a set period—usually 1 to 10 years—at a fixed or floating interest rate. Businesses use it for one-time needs like expansion, equipment purchases, or infrastructure.

This guide covers how term loans actually work, what eligibility really comes down to, current interest rate ranges, the documents you'll need, and where a term loan fits against a working capital loan or a government-backed CGTMSE facility. Picking the wrong product for your situation is one of the most common—and most avoidable—reasons applications stall.

Most borrowers compare advertised interest rates first. Lenders compare your Debt Service Coverage Ratio (DSCR) first—your operating cash flow against your debt obligations. A strong CIBIL score paired with a DSCR under roughly 1.2x will usually get an application scaled down or declined, no matter how clean the credit history looks on paper.

How a Term Loan Works

Unlike cash credit or an overdraft—where you draw and repay against a limit—a term loan gives you the full sanctioned amount upfront with a fixed repayment schedule.

Lenders generally structure term loans by tenure:

- Short-term (up to ~1 year): Bridge funding, seasonal stock, urgent equipment repair.

- Medium-term (1–3 years): Working capital top-up, smaller machinery purchases.

- Long-term (3–10 years): Business expansion, large equipment, infrastructure, property-linked projects.

Interest and Collateral Structures

Two more choices shape the EMI:

- Fixed vs. floating rate: Fixed means the same EMI for the full tenure; floating moves with the lender's benchmark rate, so the EMI can rise or fall.

- Secured vs. unsecured: Secured loans (backed by property, machinery, or other collateral) usually carry lower rates and longer tenures; unsecured loans skip the collateral requirement but price in the lender's added risk. A CGTMSE-backed structure is a third option worth knowing about—more on that below.

Term Loan Eligibility Criteria for Businesses in India

Eligibility isn't just one number. Lenders weigh credit history, the business's own track record, and how comfortably your cash flow covers the new EMI.

The factors that carry the most weight:

- Personal credit score: Most lenders look for 700+, though this varies by lender and loan size.

- Company Credit Report / CIBIL Rank: For an existing business, this matters as much as the owner's personal score.

- Business vintage: Most lenders want at least 2–3 years of operating history; newer businesses face tighter scrutiny or need a stronger DSCR to compensate.

- Turnover and DSCR: Your declared revenue and tax filings need to plausibly support the new EMI on top of existing obligations.

- Collateral (if applicable): For secured loans, the lender values the asset; for unsecured loans, the absence of collateral is offset by stricter cash-flow checks.

Term Loan vs. Working Capital Loan vs. CGTMSE

A term loan isn't the only structure that fits a one-time funding need. Use the comparison table below to quickly map your funding need to the right product:

| Feature | Term Loan | Working Capital Loan | CGTMSE-Backed Term Loan |

|---|---|---|---|

| Best for | One-time needs (expansion, equipment, infrastructure) | Recurring, short-term cash flow gaps | MSEs needing a term loan but lacking collateral |

| Disbursal | Lump sum, upfront | Revolving limit, drawn as needed | Lump sum, upfront |

| Collateral | Often required (secured); optional for unsecured | Usually tied to receivables/stock | Government guarantee replaces most collateral |

| Typical tenure | 1–10 years | Renewed annually | Matches the underlying term loan tenure |

For a deeper dive into recurring funding, read our complete guide on Cash Credit Loan vs. Term Loan: Which One Is Right for Your Business?.

Documents Required for a Term Loan Application

Documentation requirements vary slightly by lender, but most term loan applications ask for:

- Identity and address proofs (e.g., PAN, Aadhaar, and standard KYC documents).

- Business registration proof (e.g., Udyam Registration, GST certificate, partnership deed/MOA-AOA as applicable).

- Financial statements (e.g., audited financials and Income Tax Returns, typically for the last 2–3 years).

- Bank statements (usually 6–12 months, used to verify actual cash flow against declared turnover).

- Collateral documents (property papers, machinery invoices, or other security documents, for secured loans).

If your business needs ₹10 lakh or more for expansion, equipment, or a healthcare facility upgrade, a CreditCares advisor can map your documents and DSCR against 50+ bank and NBFC products before you apply anywhere—at zero upfront fee, so there's no cost to finding out where you actually stand.

Term Loan Interest Rates in India (2026): What Actually Moves the Number

Across banks and NBFCs, secured business term loans broadly run from around 9–16% per annum, while unsecured term loans—where the lender carries more risk without collateral—typically run higher, broadly in the 14–26% per annum range. Where your business lands within that range depends on credit profile, business vintage, declared turnover, and the lender's own risk model, not on the interest rate alone.

What pulls your rate down:

- A credit score consistently above 750.

- At least 3+ years of stable, verifiable turnover.

- Offering collateral, even partial.

- A CGTMSE guarantee, where eligible—this protects the lender on the unsecured portion, which often means a better rate than a fully unsecured loan would get otherwise.

Note: Rates change with RBI policy and lender-specific risk pricing, so treat the ranges above as a planning reference, not a quote. The only way to know your actual rate is a lender's formal sanction.

(Illustrative example, not a real client case)

A diagnostic centre in Salt Lake, Kolkata, wants to add a second CT scanner to handle overflow referrals from nearby clinics. The machine costs ₹85 lakh. The centre is profitable but only 3 years old, and the founder's personal CIBIL score is a respectable 720—solid, not exceptional.

While a generic eligibility checklist might flag this as borderline, the reality is different. The lender weighs the centre's revenue per scan and its existing referral tie-ups—the cash-flow story—more heavily than the founder's personal score alone. Furthermore, a CGTMSE-backed structure can remove the need for collateral beyond the machine itself. This is exactly the kind of case where matching to the right NBFC product, rather than applying cold to the first bank that comes up, changes the outcome.

Insider Insight: Why Term Loan Applications Actually Get Rejected

Beyond a low credit score, the rejection reasons that come up most often in practice:

- DSCR doesn't clear the lender's threshold: Even a high credit score doesn't offset a cash flow that's too thin against the proposed EMI plus existing obligations.

- Bank credits don't match filed GST returns: Lenders increasingly cross-check this automatically; a gap here reads as a red flag even if the business is otherwise healthy.

- Collateral is already charged elsewhere: A CERSAI search showing an existing charge on the same asset stalls or kills an application, even if the borrower didn't realise the earlier charge was still active.

- Bank statements are too "new": A large balance that shows up only in the 1–2 months before applying, without a longer pattern behind it, reads as window-dressing rather than genuine cash flow.

- Healthcare-specific issues: Missing or lapsed clinical establishment registration, or a professional council registration that doesn't match the applicant's name, is a common, fixable reason applications get stuck in underwriting.

None of these show up on a standard eligibility checklist, which is exactly why two businesses with similar credit scores can get very different outcomes.

How to Apply for a Term Loan with CreditCares

-

1

Share your requirement

Outline your loan amount, purpose, and current documents with a CreditCares advisor.

-

2

Get matched to the right product

We scan across our network of 50+ banks and NBFCs, including CGTMSE-eligible options where collateral is a constraint.

-

3

Documentation review

We check for the gaps covered above (DSCR, GST-bank mismatch, collateral status) before submission, not after a rejection.

-

4

Application and sanction

We submit to the matched lender, with CreditCares coordinating the back-and-forth.

-

5

Disbursal

Funds are released per the lender's sanction terms.

This runs on our standard zero-upfront-fee policy—you don't pay CreditCares anything to find out what you're eligible for.

Frequently Asked Questions

Disclaimer: Interest rates, eligibility criteria, and government scheme terms (including CGTMSE) are subject to change by individual lenders and the RBI, and vary by applicant. The ranges above are for general planning only and don't constitute a loan offer; your actual terms will be confirmed in writing by the sanctioning bank or NBFC.