JanSamarth Scheme: 15 Government Loans, Eligibility Criteria and How to Apply Online

Over 41 lakh applications worth more than ₹1.06 lakh crore have been processed through JanSamarth as of early 2026 – yet most business owners either do not know which scheme fits their situation, or find their application silently rejected with no clear explanation.

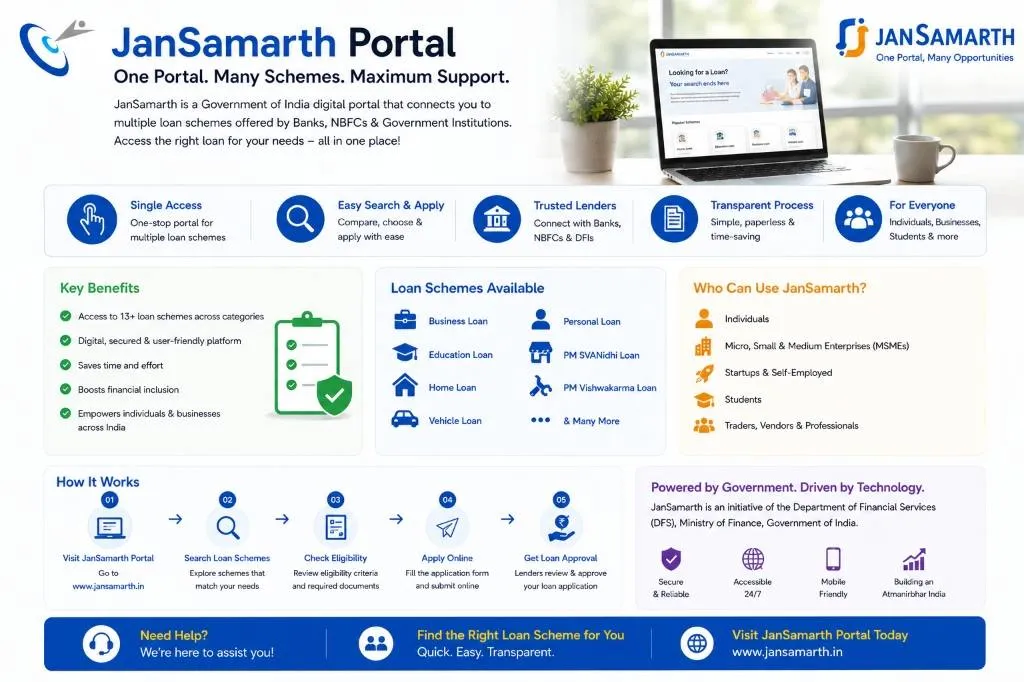

JanSamarth (jansamarth.in) is the Government of India's single-window digital portal linking 15 credit-linked central government schemes – including Mudra, PMEGP, Stand-Up India, and Kisan Credit Card – to over 250+ lenders. Applicants can check eligibility, compare offers, and receive in-principle digital loan approval without visiting a bank branch.

This guide is the complete, up-to-date reference from CreditCares on the JanSamarth scheme: every loan category available, who qualifies, what the portal does and does not cover, and when you need more than the portal can offer. For a step-by-step walkthrough of how to actually use the portal interface, see our detailed JanSamarth portal application guide.

Strategic Insight:

The JanSamarth portal is a discovery and matching engine, not a guarantee engine. It identifies the right scheme and the right lender for your profile in minutes – but whether your application is sanctioned still depends on the same credit parameters any bank uses: CIBIL score, business vintage, and debt-service capacity. Knowing which scheme to apply for is only half the equation.

What Is the JanSamarth Scheme and How Does It Work?

JanSamarth is an initiative of the Department of Financial Services under the Ministry of Finance, Government of India. Launched at jansamarth.in, the portal operates as an intelligent credit marketplace: a borrower registers once, submits their KYC and financial data, and the platform's rule engine matches them to the most appropriate government scheme and lender – automatically.

The platform integrates with UIDAI (Aadhaar), PAN, income tax return data, CIBIL, Udyam Registration, and GST portals in real time, significantly reducing the document burden compared to branch-based applications. As of mid-2026, the portal supports eight languages and is accessible via both browser and a dedicated mobile app (Android and iOS).

JanSamarth at a Glance (2026)

| Governing parameter | Details |

|---|---|

| Governing ministry | Department of Financial Services, Ministry of Finance, GoI |

| Official portal | jansamarth.in |

| Number of schemes | 15 credit-linked central government schemes |

| Number of lenders onboarded | 250+ (PSU banks, private banks, RRBs, NBFCs, SFBs) |

| Loan categories | Business / Livelihood / Education / Agriculture Infrastructure |

| Languages supported | 8 (including Hindi, Bengali, Tamil, Telugu, Marathi) |

| Applications processed to date | 41+ lakh applications, ₹1.06 lakh crore+ in value |

What the JanSamarth Portal Does Not Tell You

The portal's rule engine matches you to a scheme – it does not evaluate whether your credit profile is strong enough for that scheme's lender to actually sanction the loan. This is the gap that catches most first-time applicants: the system will accept your application for a ₹10 lakh Mudra Tarun loan even if your CIBIL score is 620, but the assigned lender will reject it at the credit appraisal stage.

Another frequently overlooked detail is that a PMEGP sanction does not equal immediate cash disbursement. After the bank sanctions your PMEGP application, the margin money (subsidy) is parked in a fixed deposit against your account for a mandatory lock-in period. The actual cash does not arrive until after verification by the implementing agency – KVIC, KVIB, or your district's DIC. Projects that skip this step or misunderstand the timeline often stall at the implementation phase.

All 15 JanSamarth Schemes – Full List with Loan Limits and Purpose

The portal organises its schemes into four loan categories. Each category targets a distinct borrower profile. Here is the complete scheme list with key parameters.

Category 1 – Business Activity Loans

| Scheme | Loan Range | Subsidy / Benefit | Who Can Apply |

|---|---|---|---|

| PMMY (Mudra) – Shishu | Up to ₹50,000 | No collateral; no guarantor | Micro / small non-farm businesses; no minimum vintage |

| PMMY – Kishor | ₹50,001 – ₹5 lakh | No collateral | Existing micro / small businesses |

| PMMY – Tarun | ₹5 lakh – ₹10 lakh | No collateral | Established micro / small businesses |

| PMMY – Tarun Plus | ₹10 lakh – ₹20 lakh | No collateral | Borrowers with clean Tarun repayment track record |

| PMEGP | Up to ₹50L (mfg) / ₹20L (services) | 15–35% subsidy on project cost (never repaid) | First-time entrepreneurs; new greenfield units only |

| Stand-Up India | ₹10 lakh – ₹1 crore | At least 1 loan per branch for SC/ST; 1 for women | SC/ST or women borrowers; greenfield mfg, services, or trading |

| PM SVANidhi | ₹10,000 – ₹50,000 | 7% interest subsidy; no collateral | Street vendors and hawkers with ULB-issued certificate |

Category 2 – Livelihood Loans

| Scheme | Loan Range | Benefit | Who Can Apply |

|---|---|---|---|

| National Livelihood Mission (DAY-NRLM) | Variable (SHG-linked) | Subsidised credit via SHG linkage | Self-Help Group (SHG) members under DAY-NRLM |

| National Urban Livelihood Mission (NULM) | Up to ₹2 lakh (indiv) / ₹10 lakh (group) | 7% interest subvention | Urban poor; SHGs; street vendors (ULB certified) |

Category 3 – Education Loans

Note on education schemes: These are interest subsidies, not free grants. You take a regular education loan from a bank; the government reimburses the interest component during your study period and moratorium. Principal repayment remains your responsibility.

| Scheme | Benefit | Who Can Apply |

|---|---|---|

| Central Sector Interest Subsidy (CSIS) | Full interest subsidy on education loan during moratorium | Students from economically weaker sections pursuing technical/professional courses in India |

| Dr. Ambedkar Central Sector Scheme | Interest subsidy during moratorium on overseas education loans | OBC and EBC students pursuing Masters or PhD abroad |

| Padho Pardesh | Interest subsidy on overseas education loans during moratorium | Minority community students for Masters / PhD abroad |

Category 4 – Agriculture Infrastructure Loans

| Scheme | Loan / Benefit | Who Can Apply |

|---|---|---|

| Agriculture Infrastructure Fund (AIF) | Up to ₹2 crore per project; 3% interest subvention | FPOs, PACS, agri-entrepreneurs, SHGs |

| ACABC | Up to ₹20 lakh (individual) / ₹1 crore (group); 36–44% subsidy | Agriculture graduates setting up Agri Clinics/Business Centres |

| Kisan Credit Card (KCC) | Revolving credit at ~7% p.a. | Farmers, fishermen, animal husbandry borrowers |

JanSamarth Eligibility – Who Can Apply for Which Scheme

Eligibility for each JanSamarth scheme depends on your borrower category. The tables above serve as a quick-match guide; the portal's own eligibility checker provides the definitive check for your specific profile.