PMEGP Scheme 2025–26: The Insider's Guide to MSME Subsidy Loans

Between April 2017 and February 2018, over four lakh young Indians applied for loans under the PMEGP scheme. Banks rejected more than 88% of those applications. The scheme promised up to ₹25 lakh in project funding with a government subsidy. Yet, barely 12% of applicants received it.

That rejection rate is still a reality today. Consultants working with MSME applicants across West Bengal and the rest of India see the same pattern playing out in 2025–26.

The PMEGP scheme is genuinely powerful — but only for applicants who understand how it actually works, rather than how the brochure describes it.

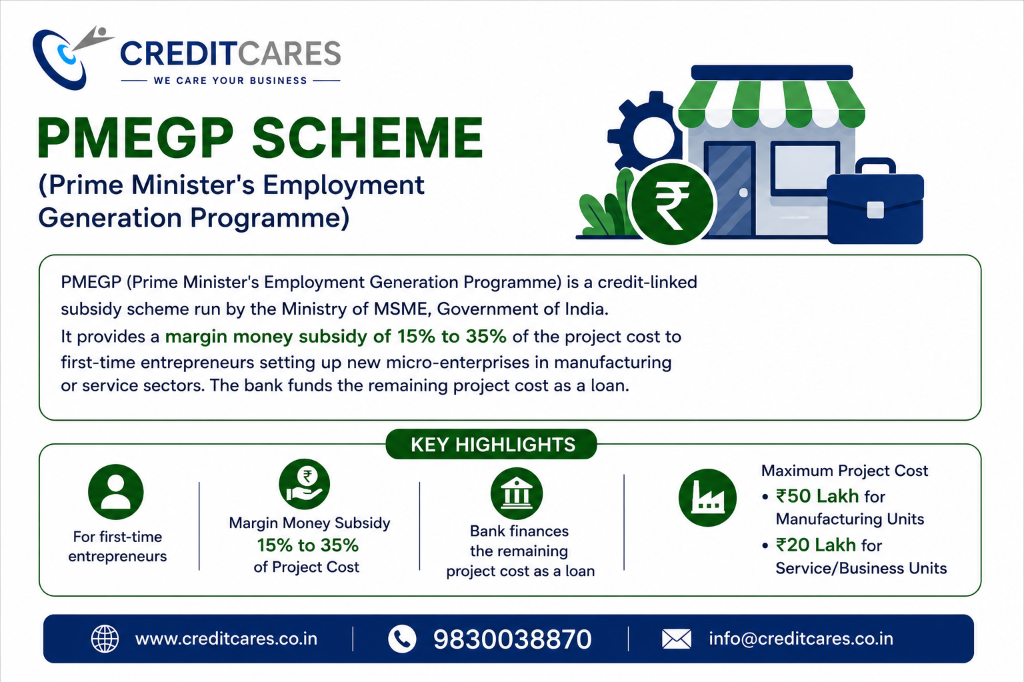

PMEGP (Prime Minister's Employment Generation Programme) is a credit-linked subsidy scheme run by the Ministry of MSME, Government of India. It provides a margin money subsidy of 15% to 35% of the project cost to first-time entrepreneurs setting up new micro-enterprises in the manufacturing or service sectors. The bank funds the remaining project cost as a loan. The maximum project cost eligible for subsidy is ₹50 lakh for manufacturing units and ₹20 lakh for service or business units.

Since its inception in 2008–09 (by merging the Prime Minister's Rojgar Yojana and the Rural Employment Generation Programme), PMEGP has supported over 9.86 lakh units and generated 80.52 lakh jobs. The scheme is implemented at the national level by KVIC (Khadi and Village Industries Commission), and at the state/district level by State KVIC Directorates, Khadi and Village Industries Boards (KVIBs), and District Industries Centres (DICs) — including the West Bengal Khadi and Village Industries Board (WBKVIB) and district DICs across the state.

The subsidy is not free money paid to you upfront. It is held by the bank as a Term Deposit Receipt (TDR) for a three-year lock-in period. Only if your unit is operational and your loan repayment is regular at the end of that period does the bank adjust the subsidy against your outstanding principal. Applicants who understand this from day one plan their cash flow and repayment very differently from those who expect a subsidy credit on day one.

How does the PMEGP subsidy actually work?

Under PMEGP, the government provides a margin money subsidy on the project cost — not on the full loan. The bank sanctions 90% of the project cost for general category applicants (95% for special category). The government releases the subsidy into the locked TDR account linked to the loan.

A detailed example makes this concept easier to understand:

Scenario: A first-generation entrepreneur in Bankura district wants to set up a carved wooden furniture-making unit (manufacturing). He belongs to the general category and the unit will be in a rural area.

| Component | Calculation | Amount |

|---|---|---|

| Total project cost | — | ₹40,00,000 |

| Own contribution (10% of project cost) | 10% × ₹40L | ₹4,00,000 |

| Government subsidy (25% for general + rural) | 25% × ₹40L | ₹10,00,000 |

| Bank loan (remaining 65%) | ₹40L − ₹4L − ₹10L | ₹26,00,000 |

| What you actually repay | — | ₹26,00,000 |

The subsidy works as a meaningful reduction on your repayable principal. You are not repaying the full project cost — you are repaying the loan portion, which is the project cost minus your own contribution and the government subsidy. That is a meaningful difference in your monthly EMI and total interest outgo.

Note: The subsidy is adjusted only after the 3-year lock-in. If the unit discontinues operations or there are serious loan defaults in those three years, the subsidy may be recovered.

PMEGP eligibility criteria 2026

Any Indian citizen above the age of 18 setting up a new micro-enterprise in manufacturing or service sectors is eligible for PMEGP. The unit must be genuinely new — existing businesses already receiving subsidy under any government scheme are not eligible.

| Eligibility Criterion | Requirement |

|---|---|

| Citizenship | Indian citizen only |

| Age | Minimum 18 years (no upper limit) |

| Enterprise type | New micro-enterprise only — not for existing running units |

| Activity | Manufacturing or service (permitted activities only) |

| Educational qualification | Class 8 pass (for projects above ₹10L manufacturing / ₹5L service) |

| Prior subsidy | Must not have previously availed PMEGP or other central/state subsidy |

| Loan default | No existing NPA with any bank or financial institution |

| Family unit | Only one member per family is eligible |

PMEGP subsidy rates and project cost limits

The PMEGP subsidy percentage depends on two factors: the applicant's social category and whether the project is in a rural or urban area. It ranges from 15% to 35%.

| Category | Urban subsidy | Rural subsidy |

|---|---|---|

| General (open category) | 15% | 25% |

| Special (SC/ST/OBC/Women/Ex-servicemen/PwD/Minorities/NER/Hill/Border areas) | 25% | 35% |

Project cost ceilings (2025–26 revised limits): ₹50 lakh for Manufacturing, ₹20 lakh for Service/Business. If the total project cost exceeds these limits, the balance credit can be availed from banks without any government subsidy.

Note for existing units: Existing PMEGP, REGP, or MUDRA units that are performing well can apply for a second loan for upgradation (up to ₹1 crore for manufacturing and ₹25 lakh for service units).

Banks are commercial lenders. They consider creditworthiness, repayment ability, and project viability. PMEGP does not override these banking conventions — it provides a subsidy on top of a normal commercial loan. Here are the actual reasons applications fail:

- A weak Detailed Project Report (DPR): The single biggest cause of rejection. Most applicants present a simple project summary. Banks need detailed financial projections, credible demand analysis, clear capacity utilisation assumptions, and machinery specifications. A generic internet template signals that the applicant has not thought through the business.

- Land cost included in the project cost: Automatic rejection. Land cost cannot be included in the project cost under PMEGP.

- CIBIL score below the cut-off: Most public sector banks will reject an application if the CIBIL score is below 650. Clear defaults and build your score to 700+ before applying.

- Own contribution not visible: You must demonstrate that your 5% or 10% contribution is available in your bank account before sanction.

- Wrong bank branch: Applying to a branch near your residence instead of the branch geographically closest to the project location results in administrative rejection.

- EDP training delays: The 14-day EDP training certificate must be available at the point of disbursement. Delays here can cause the sanction to lapse.

- Prohibited activities: Selecting an activity from the negative list. Prohibited activities include:

- Meat (slaughtered) processing

- Production or sale of intoxicants (e.g., beedi, paan, cigars, cigarettes, liquor)

- Cultivation of crops or plantation activities (tea, coffee, sericulture, floriculture)

Worked examples: A Bankura artisan and a Siliguri food processor

A male SC-category applicant from Kotulpur, Bankura, wants to set up a carved wood and artistic furniture-making unit with a project cost of ₹4,00,000. He applies through KVIC. His subsidy rate is 35% (special category, rural). Government subsidy: ₹1,40,000. Own contribution (5%): ₹20,000. Bank loan: ₹2,40,000. The unit is eligible. His DPR specifies three steady local buyers, a working capital cycle of 45 days, and a sourced cost estimate. The bank approves.

A woman applicant (special category, urban) wants to set up a small pickle and papad processing unit in Siliguri with a ₹18 lakh project cost. Her subsidy rate is 25% (special + urban). Government subsidy: ₹4,50,000. Own contribution (5%): ₹90,000. Bank loan: ₹12,60,000. The application cites confirmed orders from two local wholesale grocers and includes FSSAI registration. With a CIBIL of 720 and matching KYC documents, the file sails through.

How to apply for PMEGP online: Step by Step

-

1

Check activity eligibility

Confirm your activity is not on KVIC's negative list.

-

2

Prepare your Detailed Project Report (DPR)

Include market demand, capacity utilisation, capital expenditure breakup, projected P&L, DSCR, and repayment schedule.

-

3

Fix your KYC documents

Your name and address must match exactly across Aadhaar, PAN, and bank passbook. Even a minor variation ('Ram Prasad' vs 'R. Prasad') causes KYC failure.

-

4

Show own contribution

Keep the required 5% or 10% in your account.

-

5

Apply online

Visit kviconline.gov.in/pmegpeportal. Upload documents and select the correct implementing agency and branch.

-

6

Attend the DLTFC review

The District Level Task Force Committee will review the application (usually within 45 days).

-

7

Complete EDP training

Mandatory 14-day training after DLTFC clearance.

-

8

Bank appraisal and sanction

The bank conducts due diligence and sanctions the loan.

-

9

Start operations

KVIC conducts physical verification.

Frequently Asked Questions

Disclosure: This content is for general informational purposes only and does not constitute financial or legal advice. PMEGP scheme guidelines, subsidy rates, project cost limits, and eligibility conditions are set by the Government of India (Ministry of MSME) and are subject to revision. Always verify current terms at kviconline.gov.in or with your nearest KVIC/KVIB/DIC office before making any borrowing or investment decision. CreditCares is a loan consultancy and does not itself provide government subsidies, make lending decisions, or guarantee PMEGP approval.