PM Vishwakarma Scheme 2026: Eligibility, Loan Amount & How to Apply

Nearly 2.7 crore artisans have applied for the PM Vishwakarma scheme since it launched in 2023, but only about 4.7 lakh of them have actually received a loan tranche so far. That gap – not the headline benefits – is the part most guides to this scheme skip.

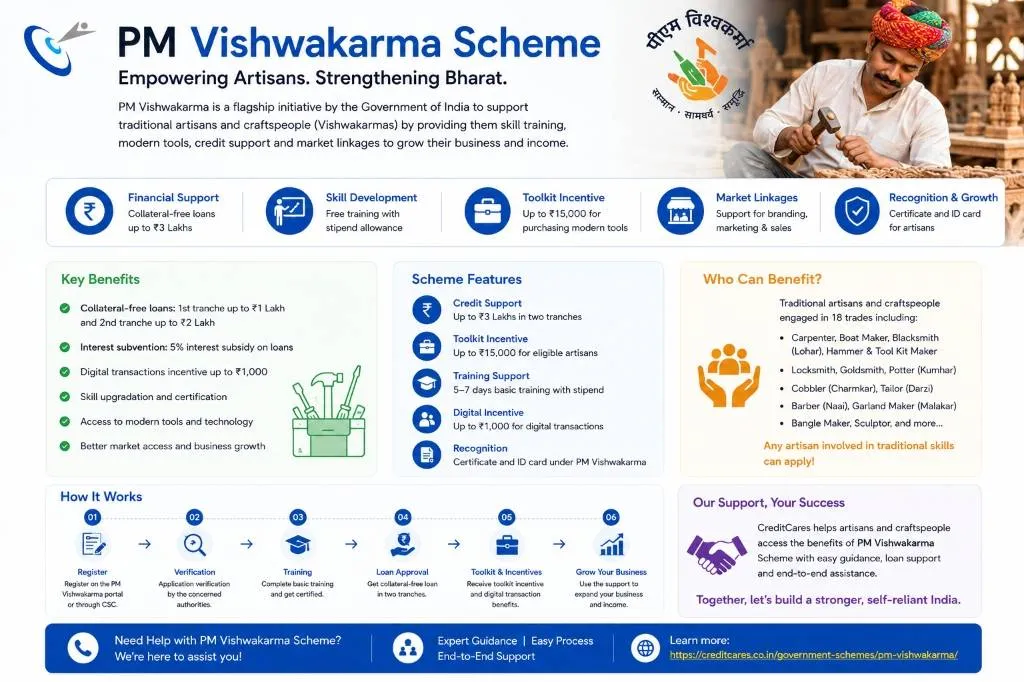

PM Vishwakarma is a Central Sector Scheme of the Ministry of MSME designed to support traditional artisans and craftspeople. It provides workers – such as carpenters, potters, blacksmiths, and tailors – with a formal ID, free skill training paired with a daily stipend, and a ₹15,000 toolkit grant. Crucially, it also opens the door to a collateral-free loan of up to ₹3 lakh at 5% interest. The initiative was launched on 17 September 2023 and runs through FY 2027-28 with a ₹13,000 crore outlay.

This guide covers exactly who qualifies, how much you can actually borrow, and the documents a Common Service Centre (CSC) will ask for. Because it matters more than most articles admit, we will also explain why a meaningful share of applications still do not convert into a disbursed loan, and what you need to check before walking into a CSC.

Strategic Insight:

Most people treat PM Vishwakarma as one scheme with one outcome. In practice, it involves three separate approvals stacked on top of each other: registration, skill verification, and loan sanction. Each stage has its own drop-off point. Knowing which stage you are at changes what you should be doing next.

What Is the PM Vishwakarma Scheme?

The PM Vishwakarma scheme provides self-employed artisans in 18 traditional trades with formal recognition and financial backing. Run jointly by the Ministry of MSME, the Ministry of Skill Development and Entrepreneurship, and the Department of Financial Services, the program onboards every beneficiary onto the Udyam Assist Platform. This registers them as a recognized MSME entrepreneur, which is vital if the artisan ever wants to graduate to a larger business loan in the future.

The scheme was launched by the Prime Minister on Vishwakarma Jayanti (17 September 2023) from Yashobhoomi in Dwarka. It runs for five years, targeting 30 lakh registered beneficiaries – a milestone the scheme has already reached.

Who Is Eligible for PM Vishwakarma?

You qualify if you are 18 or older, self-employed in the unorganized sector, work with your hands and tools in one of the 18 listed trades, and have not taken a loan under PMEGP, MUDRA, or PM SVANidhi in the last five years (unless fully repaid). Only one person per family can register, and government employees and their immediate families are strictly excluded.

The Full Eligibility Checklist:

- Minimum age of 18 years on the date of registration.

- Self-employed in the unorganized sector (not a salaried worker).

- Actively engaged in the trade at the time of registration.

- Belongs to one of the 18 family-based traditional trades.

- No active credit under PMEGP, MUDRA, or PM SVANidhi from the past 5 years.

- Only one member per family (husband, wife, unmarried children) can register.

- Not a government employee (nor an immediate family member of one).

The 18 Trades Covered

| Wood & Metal Work | Clay, Stone & Leather | Textiles & Services |

|---|---|---|

| Carpenter (Suthar/Badhai) | Potter (Kumhaar) | Tailor (Darzi) |

| Boat Maker | Sculptor/Stone Breaker | Barber (Naai) |

| Armourer | Cobbler/Shoesmith | Washerman (Dhobi) |

| Blacksmith (Lohar) | Mason (Rajmistri) | Garland Maker (Malakaar) |

| Hammer & Tool Kit Maker | Basket/Mat/Broom Maker | Fishing Net Maker |

| Locksmith & Goldsmith | Doll & Toy Maker | - |

Note: If your trade is not on this list, PM Vishwakarma is not the right fit. A MUDRA or standard MSME working capital loan will be a better alternative.

PM Vishwakarma Loan Amount, Interest Rate & Tenure

The loan is provided in two tranches totaling ₹3 lakh. Both come at a flat 5% interest rate, with the government covering an 8% subvention on top of what you pay. No collateral or third-party guarantee is required.

| Feature | Tranche 1 | Tranche 2 |

|---|---|---|

| Loan Amount | Up to ₹1,00,000 | Up to ₹2,00,000 |

| Tenure | 18 months | 30 months |

| Interest Rate | 5% p.a. | 5% p.a. |

| Subvention | Up to 8% | Up to 8% |

| Eligibility | Completion of Basic Training | Tranche 1 utilized + clean repayment record |

These loans are disbursed through Scheduled Commercial Banks, Regional Rural Banks, Small Finance Banks, Cooperative Banks, NBFCs, and Microfinance Institutions.

Documents Required for Registration

You do not need elaborate paperwork. A CSC will simply ask for:

- Aadhaar card

- Active mobile number (must be linked to Aadhaar for e-KYC)

- Bank account details (the CSC can help you open one if needed)

- Ration card (or the Aadhaar cards of all family members if you do not have a ration card)

How to Apply for the PM Vishwakarma Scheme

Registration is entirely free and happens through your nearest Common Service Centre (CSC). A Village Level Entrepreneur (VLE) operator completes your Aadhaar-based biometric registration on the official portal. You do not need to do this online yourself.

Visit the CSC

Bring your Aadhaar, mobile phone, and bank details.

Verification

The operator selects "CSC – Register Artisans" and completes your Aadhaar e-KYC.

Submission

Your Artisan Registration Form is submitted, simultaneously registering you on the Udyam Assist Platform.

Three-Stage Verification

The application is vetted at the Gram Panchayat/Urban Local Body level, the District Implementation Committee, and finally a Screening Committee.

Certification

Once approved, download your PM Vishwakarma Digital Certificate and ID Card.

Training

Complete Basic Training (5–7 days, paid via stipend) to unlock the first loan tranche. Advanced Training unlocks the second.

Note: Never pay anyone who promises faster approval outside the official process.

Worked Example: A Kumartuli Potter

Take a clay-idol-making unit in Kumartuli, Kolkata. The seasonal nature of the work—intense demand before Durga Puja, quiet stretches otherwise—is exactly where the scheme's structure matters. Tranche 1's ₹1 lakh over 18 months works well for buying clay and basic tools ahead of the season. However, a potter relying purely on festival income needs to plan their monthly EMI repayments around the off-season cash flow gap. This is a practical reality that a generic "₹1 lakh at 5%" headline rarely warns you about.

Insider Insight: Why Applications Stall Before the Loan Stage

Around 30 lakh artisans have been registered, but only about 4.7 lakh have received a sanctioned loan. Public sector banks flagged the main reason: applicants who already took a loan under PMEGP or MUDRA in the past five years, or applicants with an active NPA (non-performing asset) flag on their credit history. It is rarely about the artisan's skill; it is a paperwork disqualification. Ensure any previous government loans are fully settled before applying.

What Happens After Your PM Vishwakarma Loan?

₹3 lakh is enough to modernize tools and stabilize a one-person trade, but it is not designed to fund major expansions, such as a tailor adding heavy machinery or a mason taking on large commercial contracts.

If you have repaid your PM Vishwakarma tranches and now need ₹5–50 lakh for machinery or expansion, that is a conversation CreditCares specializes in. We structure CGTMSE-backed collateral-free loans, working capital facilities, and MSME loans for growing businesses across our 50+ banking and NBFC partners.