Stand-Up India Scheme: Eligibility, Loan Amount & How to Apply

Most entrepreneurs who get turned away from Stand-Up India aren't rejected due to paperwork. Often, they were never eligible to apply in the first place, but nobody told them before they spent weeks preparing a file.

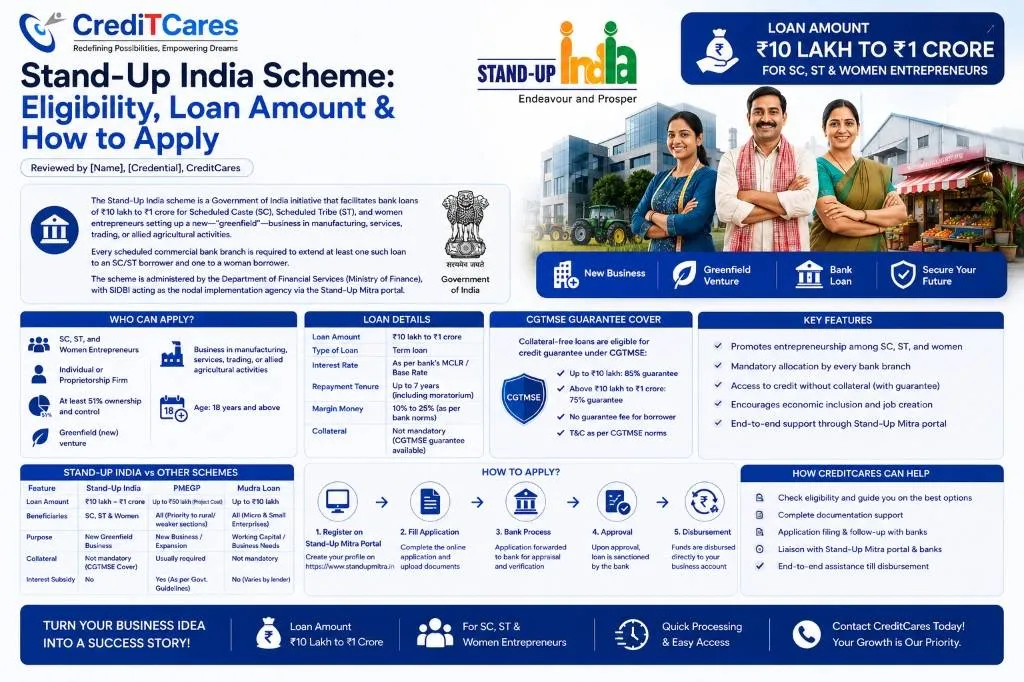

The Stand-Up India scheme is a Government of India initiative that facilitates bank loans of ₹10 lakh to ₹1 crore for Scheduled Caste (SC), Scheduled Tribe (ST), and women entrepreneurs setting up a new—"greenfield"—business in manufacturing, services, trading, or allied agricultural activities. Every scheduled commercial bank branch is required to extend at least one such loan to an SC/ST borrower and one to a woman borrower. The scheme is administered by the Department of Financial Services (Ministry of Finance), with SIDBI acting as the nodal implementation agency via the Stand-Up Mitra portal.

This guide covers who actually qualifies, how the loan and guarantee work, how the scheme compares to PMEGP and Mudra, and how CreditCares can help with the hardest parts: the project report and bank coordination.

The single biggest reason applications stall isn't the loan amount or the interest rate—it is the greenfield test. If you have operated any similar business before, even informally, you do not qualify, no matter how strong your project looks. Checking this first saves weeks of effort.

Who Actually Qualifies for Stand-Up India?

Eligibility requires you to be an SC, ST, or woman entrepreneur, above 18, starting a first-time business. You cannot be expanding, rebranding, or taking over an existing one. For non-individual entities (partnerships, companies, cooperatives), at least 51% of the shareholding and controlling stake must be held by SC/ST individuals or women.

Beyond that:

- The proposed business must fall under manufacturing, services, trading, or allied agricultural activities.

- You must not have defaulted on any existing loan with a bank or NBFC.

- Only one loan is permitted per family for setting up or acquiring a business unit.

Beyond the greenfield test, three things slow down otherwise-qualified applicants:

- Branch-level quota confusion: The "one SC/ST and one woman borrower per branch" mandate is a minimum, not a cap. However, some branches treat it as already fulfilled for the year and redirect applicants elsewhere. A different branch or a Lead District Manager (LDM) referral usually resolves this.

- Project report quality: First-time entrepreneurs, by definition, have no operating history for the bank to underwrite against. A weak or generic project report is the most common reason a genuinely eligible application gets a soft "come back later" rather than an outright rejection.

- Guarantee paperwork lag: The Credit Guarantee Scheme for Stand-Up India Loans (CGFSI), administered by NCGTC, needs to be registered correctly at the branch level. This step is sometimes missed, leaving the loan effectively uncovered until corrected.

How the Loan and Guarantee Work

Stand-Up India offers a composite loan (a single loan that combines a term loan for buying assets and working capital for daily operations) covering up to 85% of the project cost. The entrepreneur contributes a margin of up to 15% (a minimum 10% own contribution applies even where other subsidies cover part of the margin).

- Tenure: Up to 7 years, with a moratorium of up to 18 months.

- Interest rate: Set by the lending bank as the lowest rate applicable to that borrower category, capped at the bank's benchmark lending rate (MCLR/EBLR) plus 3% plus a tenor premium. This formula is fixed by the scheme, but the actual number moves with the bank's current benchmark rate. Confirm the live figure with the branch rather than quoting last year's rate.

- Security: Primary security is the assets created from the loan itself. Beyond that, collateral or a CGFSI guarantee covers the lender's risk, at the bank's discretion.

- Other features: A RuPay debit card for working capital access, and "handholding support"—structured help with training, project reports, and application filing through an associated network of agencies.

Our CGTMSE guide covers the alternative collateral-free route if you don't fit the SC/ST/women-only eligibility gate here.

Stand-Up India vs. PMEGP vs. Mudra vs. CGTMSE

These four schemes get confused constantly because they all target small, often first-time, borrowers—but they answer different situations.

| Scheme | Who It's For | Loan Range | Collateral | Subsidy/Guarantee |

|---|---|---|---|---|

| Stand-Up India | SC/ST or women, greenfield only | ₹10 lakh – ₹1 crore | Collateral or CGFSI guarantee, bank's discretion | No direct subsidy; CGFSI credit guarantee |

| PMEGP | Anyone meeting KVIC criteria, greenfield only | Up to ₹50 lakh (manufacturing) / ₹20 lakh (services) | Generally collateral-free | 15–35% capital subsidy depending on category/location |

| Mudra (Tarun/Tarun Plus) | Any non-farm micro/small enterprise, existing or new | Up to ₹20 lakh | Collateral-free | CGFMU guarantee (a different scheme from CGTMSE) |

| CGTMSE-backed term loan | Udyam-registered MSEs, new or existing | Up to ₹10 crore | None — guarantee substitutes | CGTMSE guarantee, 75–85% of lender's risk |

If you don't meet the SC/ST/women or greenfield criteria above, CGTMSE is usually the better fit. Our government schemes guide goes deeper on choosing between all four.

A woman entrepreneur in Salt Lake Sector V wants to start a small IT-enabled back-office services unit—her first business. She previously worked as an employee at a similar company, not as an owner.

This matters more than her credit profile: prior employment in the sector doesn't break the greenfield test, but prior ownership of a similar unit would. If she is bringing in a partner, the bank will also check that she holds at least 51% of the controlling stake—a detail that's easy to miss when structuring a partnership on paper.

(Illustrative scenario for explanatory purposes — not a real client case.)

Documents Required

| Category | Typical Documents |

|---|---|

| Identity & address | PAN, Aadhaar/Voter ID/Passport, recent utility bill |

| Category proof | SC/ST certificate, where applicable |

| Business | Project report, premises proof, partnership deed/MoA (for non-individual entities) |

| Financial | Bank account details, non-default declaration |

How to Apply

-

1

Register

Sign up on Stand-Up Mitra (standupmitra.in) or approach a bank branch directly—both routes are valid.

-

2

Get your eligibility checked

CreditCares can confirm the greenfield test and ownership-stake requirement before you invest time in a project report.

-

3

Project report preparation

This is where most first-time applicants need the most help. A CreditCares consultant works through this with you.

-

4

Branch coordination

Including resolving quota or LDM-referral confusion if it comes up.

-

5

Guarantee registration & disbursement

Confirming CGFSI cover is correctly recorded before the loan is treated as fully sanctioned.

CreditCares charges nothing upfront for this. We are paid a service fee by the bank only after disbursement, and we don't guarantee approval; the bank's credit decision is final.

Frequently Asked Questions

Disclaimer: Loan amounts, margin requirements, and interest rate formulas above reflect the scheme's published structure as of this writing and are subject to revision by the Department of Financial Services, NCGTC, or individual lending banks. CreditCares is a loan consultancy and DSA, not a lender. We do not guarantee scheme eligibility or loan approval; the final decision rests with the lending bank. Please verify current terms before applying.